42.5 million people have federal student loan debt in the U.S. with average monthly student loan repayments of $536, up from $503 in 2024. Two key actions have taken place in the U.S. this year that warrant taking another look at the burden of student debt and how employers can help employees manage it:

- The U.S. Department of Education made announcements earlier this year that they are resuming involuntary collections (i.e., withholding tax refunds and garnishing up to 15% of wages) for people who are behind in repaying student debt after years of various federal student debt relief efforts during and following the initial years of the COVID-19 pandemic.

- The July 2025 passage of the One Big Beautiful Bill Act (OBBBA) alters loan and repayment options as well as permanently extends certain employer student debt repayment support.

TransUnion reports that 31% of federal student loan borrowers currently in repayment are 90 days or more past due on their payments. Over five million federal student loan borrowers were in default (i.e., have not made a payment in at least 270 days) and another four million were facing imminent default as of April 2025. The newly reported delinquencies have resulted in an average 60-point drop in credit scores which further undermines borrowers’ abilities to secure housing, access credit, and maintain financial stability. These penalties are creating financial insecurity and related stress which have direct impacts on the workplace. On average, these stressors contribute to an average loss of seven hours of productivity per week for an estimated $250 billion of loss productivity annually.

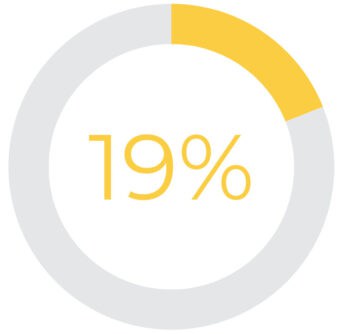

Commonwealth’s brief, The Hidden Burdens of Student Debt & The Potential of Employer-Provided Solutions, published in 2024, highlighted the significant workplace impacts of student debt on employees earning low-to-moderate incomes (LMI):

said student debt increased their financial stress

had to work additional jobs or overtime hours

tried to leave their job for another that offered higher pay or better workplace benefits

Since then, the impacts of student debt have grown significantly as default rates climb and the federal government intensifies collection efforts. The consequences extend beyond individual borrowers—as credit scores fall and financial stress intensifies, employers should expect direct impacts on employee well-being, retention, and performance.

Policy Options for Employers

SECURE 2.0

- Student Loan Retirement Match has allowed employers to match the amount an employee pays for student loans into the employee’s retirement account since January 1, 2024.

- The new rules for 529 accounts allow a maximum contribution of $10,000 during the lifetime of the beneficiary to be used to pay down student loans.

The CARES Act & OBBBA:

- The CARES Act temporarily allowed employers’ use of Section 127 Educational Assistance (i.e., tax-advantaged education contributions of up to $5,250 per employee annually) to go towards paying down employees’ student debt through December 31, 2025. The OBBBA removed the expiration date so employers can continue receiving tax benefits for helping employees pay off their student loans in 2026 and beyond.

Employers that use the policy tools and levers available to offer student debt workplace benefits will create a win-win situation for them and their employees—especially for employees earning LMI. In addition to employees yielding the benefits of paying down student loans and lessening financial stress, employers who have enacted the Student Loan Retirement Match provision saw a 58% reduction in the likelihood of employee turnover among those enrolled in 2024.

Now is the time for employers to review how to support the financial health of their workforce, including student debt support. Many assume the burden of student debt is solely an issue for younger and mid-career workers in their prime wealth-building years, but in fact, 9.3 million borrowers are 50 years old and older. When only 7.1% of borrowers typically pay off student loans within the recommended 10 years, student loan repayment ends up limiting workers’ opportunities to invest in their futures for decades of their working lives. Addressing student debt is an underutilized but high impact financial wellness solution for employers that increases productivity, attracts new talent, and improves retention.

It takes an average of 20 years to pay off student loans.

Commonwealth is here to help you take action in supporting the financial well-being of your employees by lessening the burden of student loan debt. We can partner with you to:

- Assess your employees’ financial pain points, including how student debt is impacting your employees’ well-being, productivity, and satisfaction in the workplace.

- Tailor new and existing benefit offerings and features to specifically address employees’ pain points and deeply felt needs around student loans.

- Assist you in making new and existing benefits accessible to all workers, easy to enroll in, and easy to use.

If your organization is interested in exploring how Commonwealth can optimize the communications, uptake, and impact of your workplace financial benefits—particularly with customized support for addressing employees’ student debt challenges—please click the button below.