As the COVID-19 recession pushes more and more Americans to the limits of their financial resources, retirement savings—usually considered an untouchable pool of funds—are increasingly functioning as emergency cash. With more Americans losing their jobs—and millions more losing supplemental unemployment benefits, further exacerbating income volatility—more savers will be forced to tap their 401(k)s, jeopardizing their future retirement security. COVID-19 has underscored a critical and longstanding need for short-term savings; it has also provided recordkeepers with a unique opportunity to help plan participants build the financial cushion they currently lack.

In the last several months, Commonwealth has written several posts to help recordkeepers and plan sponsors effectively build and assess emergency savings products, particularly for low- and moderate-income employees. In our latest post, we briefly discuss the differences between product types, followed by an in-depth comparison of three recordkeeper-provided products that enable employees to build emergency savings.

Recordkeeper-Provided Emergency Savings Products

Recordkeepers can help plan participants build a financial cushion by offering highly liquid emergency savings solutions structured either in-plan or out-of-plan. Both types of short-term savings products benefit recordkeepers, plan sponsors, and employees alike. Primary benefits include 1) decreased leakage in the form of hardships and loans; 2) improved employee productivity and retention; and 3) more sustainable retirement savings by employees, who can use retirement savings for retirement, not emergencies.

Recordkeepers and plan sponsors should decide which solution best meets their participants’ needs based on the various benefits and features of each savings product. For example, employees need to set up a new account with a third party to use out-of-plan solutions. In contrast, although in-plan accounts require employers to set up an after-tax account within their 401(k) plan, which only about 15% currently offer, employees can start using the solution without creating a new account and readily save via automatic paycheck deductions. Speed of withdrawal also varies widely by type of account where the funds are kept.

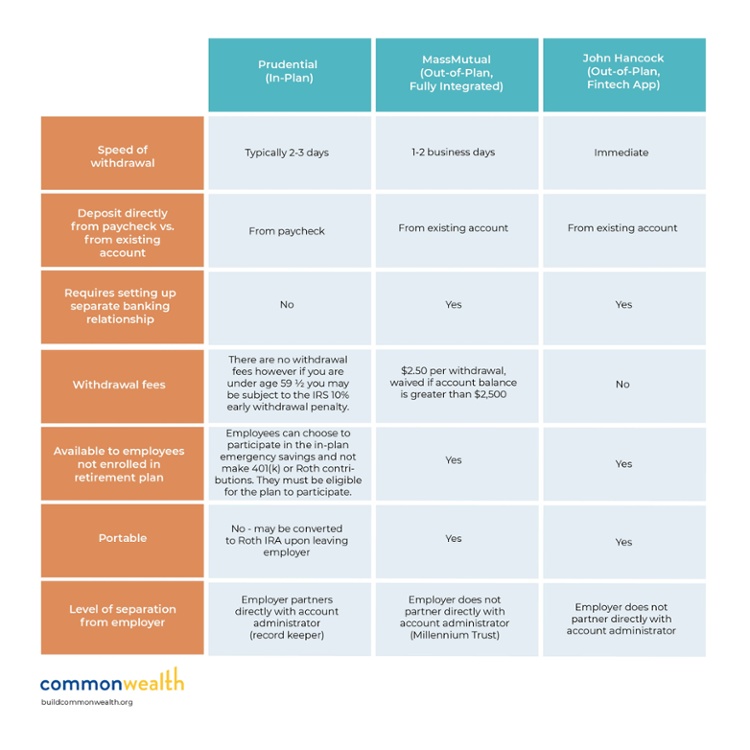

A Comparison of Three Plans

The three emergency savings tools currently available to employers come from Prudential, MassMutual, and John Hancock. In order from most to least integrated into the retirement solution, they are:

Prudential (In-Plan)

- An after-tax solution introduced in 2018 in partnership with the nonprofit Prosperity Now.

- Only the earnings are taxed (and penalized if the participant is under age 59 ½) on withdrawal due to the after-tax structure of the product.

- 135,000 employees were enrolled as of fall 2019; a broader rollout is planned for later this year.

- More than 20 clients are offering this plan, according to Christine Lange, Head of Retirement Business Management & Customer Solutions at Prudential Financial.

- She also shared that:

- Workers can automate contributions to the after-tax portion of their 401(k) account by deducting as little as 1% from their paycheck each pay period.

- Average contribution is about 4%.

- An online portal and mobile app enable employees to change their contribution rate and start or stop contributions whenever they’d like.

- About half of participants had not been making pre-tax contributions, suggesting that the after-tax product helped bring participants into Prudential’s plan.

- Employers can match the after-tax portion with no additional fee to the plan sponsor or participant.

MassMutual (Out-of-Plan, Fully Integrated)

- MassMutual partnered with Millennium Trust to introduce their solution in January 2020.

- The FDIC-insured cash account program is held by Millennium Trust and is available through MassMutual’s MapMyFinances financial wellness tool.

- The plan is available to MassMutual’s over 2.6 million retirement plan savers.

- Account holders are required to make a minimum deposit of $25 per month and are allowed a maximum balance of $250,000.

John Hancock (Out-of-plan, Fintech App)

- John Hancock made its standalone emergency savings tool available through its participant website in February 2020.

- Plan participants can access their account and set up recurring deposits from their checking account through the participant site.

- Participants are automatically enrolled in a cash account for free; they can also opt to invest in a managed account for an advisory fee.

- Participants set a savings goal within the app, track their progress, and transfer funds into their checking accounts for free.

With these three offerings, over 5.3 million Americans have access to an emergency savings product through their retirement recordkeeper—John Hancock’s product is available to nearly all of its 2.6 million participants. This number will grow as new plan sponsors offer Prudential’s solution. However, there is significant opportunity to scale further: these plan participants represent only a fraction of the 100 million Americans saving in defined contribution plans as of 2019. Millions of workers who are not saving in their employers’ 401(k) plans or who do not qualify for 401(k) plans can still access out-of-plan solutions.

A New Era for Emergency Savings

The need for these tools is not new, but the urgency of that need is: in our current COVID-19 crisis, recordkeepers and employers can offer workers one of the tools they need to make financial security possible. Supporting low-to-moderate income workers, who struggle with financial stability and resilience as a first-order challenge, is increasingly crucial as the crisis persists.

Commonwealth does not endorse any in- or out-of-plan emergency savings product. Through BlackRock’s Emergency Savings Initiative, Commonwealth and its partners are designing and deploying new emergency savings solutions with recordkeepers and plan sponsors. If you are a plan sponsor or recordkeeper interested in learning more about how to provide an emergency savings solution to your employees or plan participants, email Nick Maynard at esi@buildcommonwealth.org.